Photo by micheile henderson on Unsplash

I hope to tell you we were shocked

At the 80-year-old man found dead

…

$180,000 in grimy envelopes scattered

Everywhere like old hopes, old sin.

Regret—Michael Riley

I was touched by Michael Riley’s poem, which conflates the misery of the miser and the equally meaningless life of a rich retiree with handmade shoes. But, in a way, I relate to both unattractive images. I managed not to squander today’s pleasures in fear of having too little tomorrow – but barely. Retiring “comfortably” caused discomfort because there was something “wrong” about having a monthly income without working.

That disquiet began when I became aware of the dreaded RMD – the required minimum distribution from tax deferred retirement savings accounts….I spent hours in my late 60s using IRS tables to see whether I would have enough to live on until, in total frustration, I called Darla, who manages our money. Her response: “Yes, if you keep living the way you are. In fact, because you are retiring late, you should spend what you want now, and travel where you want to go. When you are 80, one or the other of you probably won’t want to do that anymore.” Darla is blunt.

When Karen Martha and I started this blog, we resolved to reflect on what we were thinking about (confronting? agonizing over?) as we moved from satisfying mid-life and work to something less well defined. We were also clear about what we wanted to avoid. So many retirement blogs emphasize issues of money – how much you need to have to retire, how to manage it once you have retired, and how financial decisions should affect others, such as whether to work part time or to move to a less costly city/state. We wanted, in contrast, to focus on what was in our hearts. But, money becomes unavoidable at some point.

We have much in common, but over our many years of friendship we never really delved into our unrealistic but unmanaged fear of poverty. Karen Martha grew up with a single mother in her early years, and experienced financial hardship until her mother remarried; my father went back to graduate school in his 30s and, although not poor, my parents had to watch their finances carefully. However, the Karens agree that our lessons — NEVER have any credit card debt and ALWAYS save more than necessary — were not particularly logical since we worked in education – not highly paid, but also a profession with employment security and good pensions.

Fast forward to my middle 70s: Dan and I have Social Security, and we have enough from retirement accounts to live more comfortably than anticipated. What a blessing! I have the luxury of blogging, traveling, volunteering and playing with grandchildren, and don’t anticipate much paid work. The same is true of most of my friends.

But “you worked hard for it” feels self-satisfied when newspapers report weekly that most Americans are unable to save for retirement, and others are chronically under-insured and a step away from a health-induced financial disaster. Then there is the annual “windfall” of RMD from those pre-tax retirement accounts which will, apparently, never run out. In other words, I feel guilty and even (sometimes) unworthy of being one of the “advantaged older population”.

When I was working, I adhered to my family’s legacy of prioritizing charitable donations, but there was an upper bound set by the NEVER credit card debt and ALWAYS save rules. Now, enter the late fall specter of the RMD windfall…the old messages argue in one ear that anything that I do not need this year should be reinvested so that I won’t be eating dog food when I turn 100. An equally insistent message to give away what I can afford speaks in the other ear. Then there is a new rumbling note that floats above: I was fortunate to live during a period of unprecedented economic growth and to be financially secure; my grandchildren are unlikely to have the same experience. How much should I be saving for them?

Peter Singer has one answer in Famine, Affluence, and Morality: We all, within our means, have a moral obligation to reduce suffering, and owe this to all people and places because of our common humanity. But his argument ignores every parent’s obligation to protect our loved ones from realistically anticipated harms. The Native American 7th generation principle also requires me to attend to the suffering of the planet and all of the creatures and plants that make our home livable. And what about the international movements to create peace and stability in our fragile social systems? Or initiatives that support flourishing as well as alleviating suffering (e.g., youth programs)? Oh, the causes that I feel drawn to – and the guilt that I feel when deleting requests for contributions from groups that “do good” and are highly rated by Charity Navigator….

RMD sits there in the middle: I have to take it and pay incomes taxes according to the government. Then – SAVE for Dan and me, SAVE for the coming disasters that will occur in 50 years, SAVE for unaffordable college tuition for the next generation, or DONATE now.

So, although I said that I would never, never be one of those retired people who perseverate about money even though they have more than enough, I find that I cannot avoid the subject.

And lifelong frugality kicks in…should we take that long-postponed Viking River Cruise? (Yikes! Have you seen what they cost for a room that has a view?) Should I feel depraved because we bought an upscale (used) car when the food bank sends me letters every month? And what about my alma mater, which has a decent endowment but would like more for scholarships?

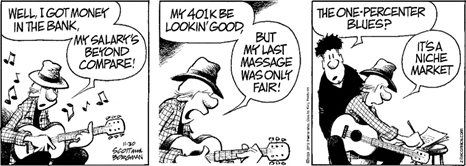

The gift of being affluent and older – definitely not in the 1% — is a niche market. Until now, I have not had to think about the sardonic message of the cartoon below but it makes me uncomfortable. When I was saving and young/middle aged, I would have viewed the message as political. Now I have to ask if it is personal….